European tourism continued to demonstrate resilience during the first half of 2026, with international tourist arrivals rising by 5% despite mounting geopolitical tensions, economic uncertainty and growing pressure on household budgets.

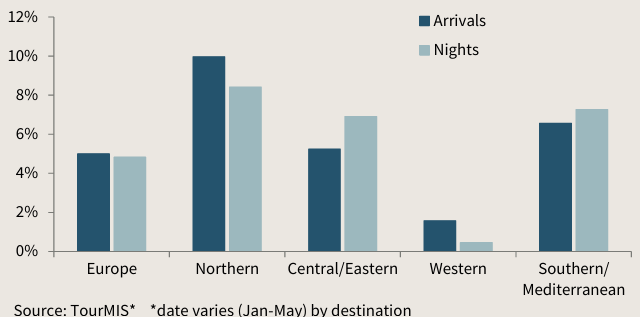

According to the latest European Tourism: Trends & Prospects report published by the European Travel Commission (ETC), international tourist arrivals across Europe increased by 5.0% year-to-date compared with the same period in 2025, while overnight stays rose by 4.8%.

The figures indicate that travel remains a priority for consumers, even as travellers become increasingly selective about where, when and how they holiday. Safety, affordability, value for money and proximity are playing a greater role in destination choice, while travel is becoming more evenly distributed throughout the year.

Most European destinations continue to grow

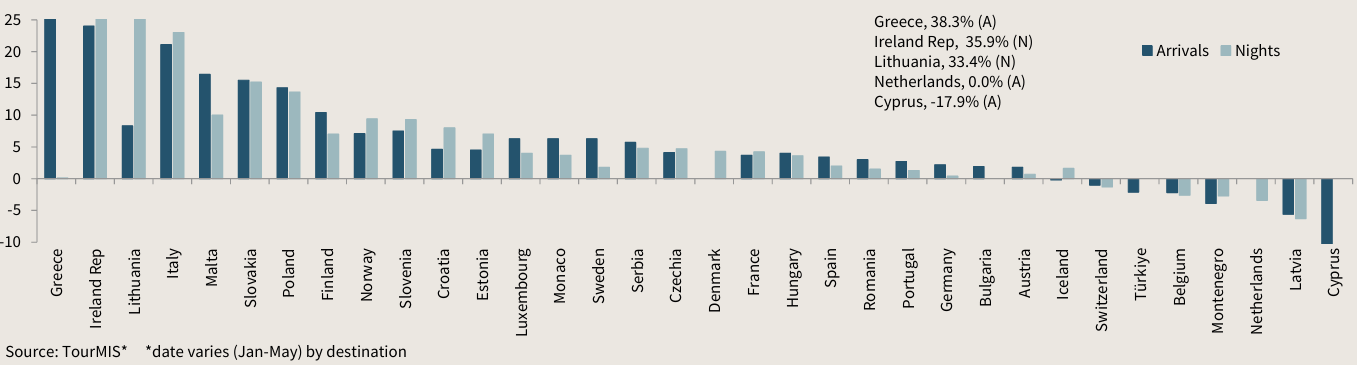

Tourism growth remained broad-based across Europe, with almost 80% of reporting destinations recording increases in international arrivals and around one in five posting double-digit growth.

Greece emerged as Europe’s strongest performer, welcoming 38% more international visitors than during the same period last year. Italy followed with a 21% increase, while Malta recorded growth of 16%, supported by improved air connectivity and efforts to spread demand beyond traditional hotspots and the peak summer season.

Northern Europe outperformed every other subregion, with arrivals increasing by 10% and overnight stays by 8.4%. Central and Eastern Europe also posted healthy gains, with arrivals rising by 5.2% and nights by 6.9%, reflecting growing demand for destinations offering fresh experiences and better value for money.

Southern and Mediterranean Europe continued to deliver solid results in absolute terms, with broad-based growth across destinations including Greece, Italy, Malta, Portugal and Spain.

Conflict in the Middle East disrupts aviation

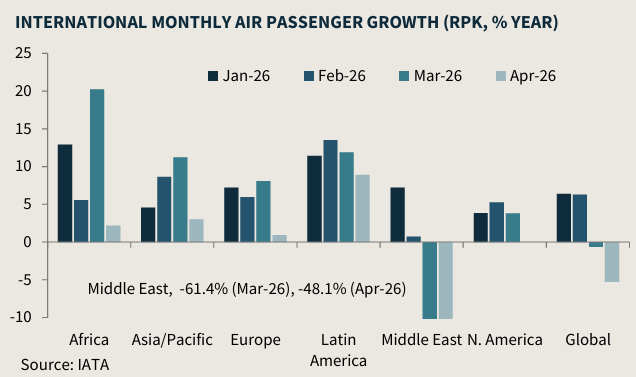

Despite the positive overall picture, the report highlights the impact of ongoing conflict in the Middle East on parts of Europe’s tourism sector.

Disruption to air routes between Europe and several mid-haul and long-haul markets slowed aviation growth during the second quarter. European airlines recorded a 7% increase in Revenue Passenger Kilometres during the first quarter of 2026, but growth fell sharply to just 1% in April as regional instability affected flight operations.

Some destinations also experienced weaker tourism performance. Cyprus saw international arrivals decline by 17.9%, partly due to Easter calendar effects but also because of travellers’ concerns about the island’s perceived proximity to the conflict.

Türkiye likewise recorded a 2.1% decline in arrivals, reflecting softer demand from both European and long-haul markets.

Visitor spending generally outpaced arrivals

Travel expenditure increased faster than visitor numbers in many destinations, suggesting that average spending per visitor has risen compared with last year.

Greece again stood out, with tourism receipts increasing by 64.3% alongside a 38.3% rise in arrivals, indicating significantly higher spending per trip.

Italy presented a different picture. Although arrivals grew by 21.1%, travel spending increased by just 4.3%, pointing to lower average expenditure per visitor despite strong demand.

Cyprus and Türkiye were among the few destinations where both visitor numbers and tourism receipts declined.

Value, safety and flexibility shape travel choices

For the rest of 2026, ETC expects leisure travel demand to remain robust despite continued economic uncertainty.

Consumer spending on leisure travel across Europe’s main source markets is forecast to remain stable at around 13% of total household expenditure this year, well above the global average of 8.5%.

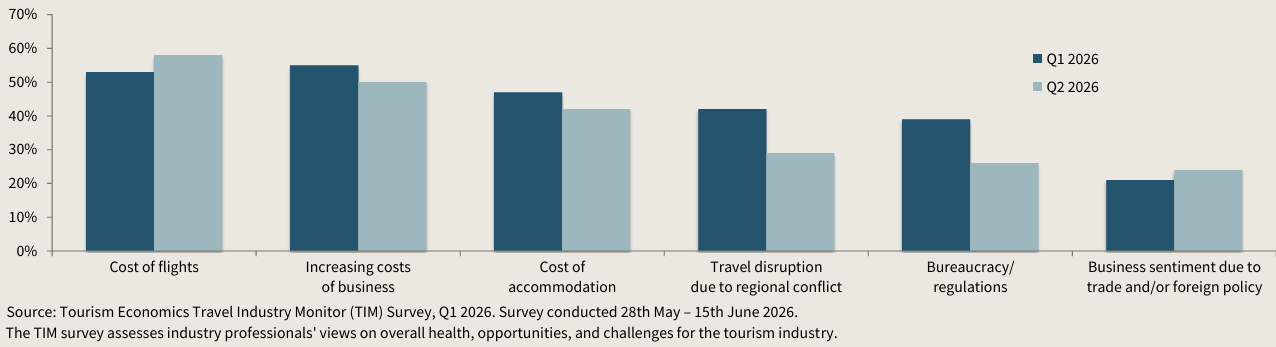

At the same time, travellers are becoming increasingly price-sensitive. According to ETC’s latest Travel Industry Monitor, 48% of respondents identified affordability and value for money as one of Europe’s key competitive advantages during the second quarter, up from 32% in the first quarter.

Destinations offering competitive prices, easy accessibility and flexibility are therefore expected to perform particularly well during the summer and autumn travel seasons.

Travellers are also increasingly favouring destinations closer to home. Interest in Southern and Mediterranean Europe for trips between June and November has risen to 61%, while shoulder-season travel continues to gain momentum as visitors seek to avoid overcrowding and increasingly frequent episodes of extreme heat.

Trends reinforce changing traveller behaviour

The latest findings reinforce trends identified in ETC’s recent Monitoring Sentiment for Intra-European Travel survey, previously reported by Travel Tomorrow, which found that 81% of Europeans intend to travel between June and November despite geopolitical and economic uncertainty.

That survey showed travellers increasingly prioritising safety, affordability and climate considerations when choosing destinations. It also found growing interest in lesser-known locations and travel outside the traditional peak summer period, with many visitors seeking quieter experiences and greater flexibility.

Interest in sustainable tourism also continues to grow. Google Trends data show rising searches for sustainable tourism in 2026 compared with the previous year. However, ETC notes that awareness has yet to translate fully into behaviour, with only 41% of consumers saying environmental concerns are likely to influence how they travel.

Commenting on the report, Miguel Sanz, President of the European Travel Commission, said European tourism had continued to demonstrate resilience despite an increasingly uncertain global environment.

“Travel remains a priority for consumers, but the way people travel is changing,” he said. “Affordability, safety, proximity and value for money are becoming increasingly important in destination choice. For European destinations, the priority is to remain competitive while supporting more balanced visitor flows across regions and seasons.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}