Back in April, I wrote here about the new methodology that the ICRT global has developed with colleagues in southern Africa to reliably report on the local economic impact of a tourism accommodation business. Signed off by the accountant used to submit your annual accounts, this offers so much more than certification. Real data on local spend and wages – are you paying more than the national minimum wage?

Within the Responsible Tourism Movement, we have not talked much about taxation. One of the most extractive forms of tourism is short-term rentals, where the owner rents a home out as a holiday let and does not reside and pay tax locally. If a Londoner owns a second home in Wales or Portugal and banks the rent in London, the local economic benefit will be limited to payments to the cleaner and a little maintenance. If renting out a property in Wales, there is a good chance that UK tax will be taken. If the rental property is in Portugal, there is a good chance that the UK taxman will not take a cut and Portugal certainly won’t.

When we applied the ICRT Global’s “economic benefit” methodology to Piggs Peak Hotel in Eswatini, formerly Swaziland, we were able to report that it paid 5,242,525 Emalangeni, 281,000 Euro, in taxes and levies to government, most of which would amount to a local economic benefit.

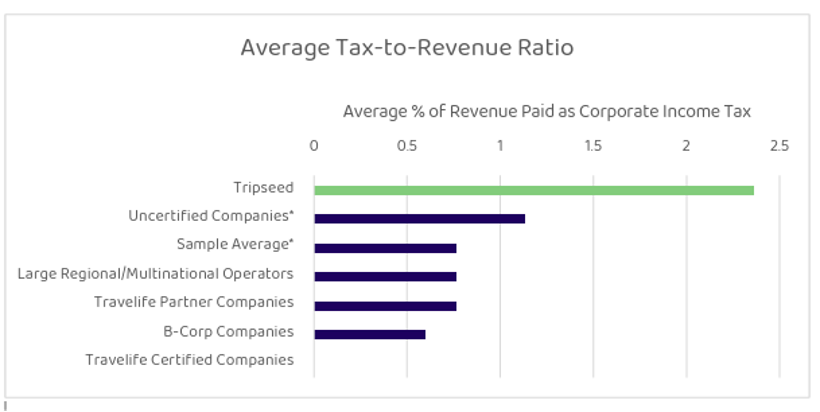

Ewan Cluckie of Tripseed and ICRT Thailand has gone further. Ewan analysed a sample of 17 well-known destination management companies and tour operators in Thailand, revealing significant variation in tax practices.

As Ewan points out:

“This data reveals a troubling paradox warranting further research: companies without sustainability certifications are, on average, contributing a higher amount to Thailand’s public finances (proportionally to their revenue share within our anonymised sample – 1.13% Tax-to-Revenue Ratio) than those with prestigious international sustainability certifications. In this sample, certification status shows a negative association with tax-to-revenue ratios. We do not infer causation and note potential confounders such as credits, loss carry-forwards, consolidation, or timing.”

Ewan rightly points out that Thailand’s ability to invest in managing tourism impacts and build resilience requires funding from taxation or levies.

A couple of weeks ago, Tripseed became the first company in the world to be accredited under the Fair Tax Foundation’s new National Business Standard for the Fair Tax Mark. An independent accreditation that recognises businesses paying the right amount of corporation tax, in the right place, at the right time, and being transparent about how they do it. It isn’t a logo you can buy or a pledge you can sign. It’s an assessment of how a business is structured, governed and taxed, checked against a published standard.

Will other businesses follow?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}