The International Air Transport Association (IATA) has released data showing that global passenger demand has fallen, with international air travel dropping more than domestic journeys. The figures are in line with other reports indicating that travellers are staying closer to home since the outbreak of hostilities in the Middle East in February 2026 amid what IATA’s Director General Willie Walsh described as a “highly volatile” situation for aviation.

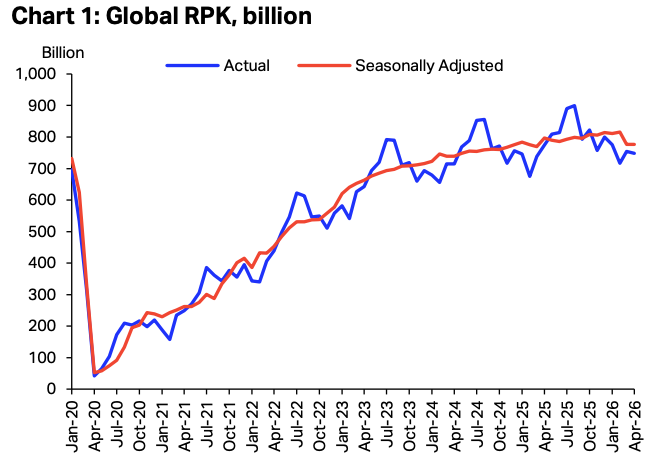

The data, for April 2026, shows that total demand declined 3.4% compared to the same month last year. Excluding the Middle East, demand in fact increased by 1.2%. Total capacity, measured in available seat kilometres (ASK), decreased 2.9% year-on-year. The load factor was 83.1% (-0.4 ppt compared to April 2025).

International impact of jet fuel costs

International demand fell 5.3% compared to April 2025. Excluding the Middle East, demand grew by 1.9%. Capacity was down 5.1% year-on-year, and the load factor was 83.9% (-0.2 ppt compared to April 2025). Meanwhile, domestic demand did not fall but stagnated compared to April 2025. Capacity increased 0.8% year-on-year. The load factor was 81.9% (-0.7 ppt compared to April 2025).

“The 46.6% fall in demand for carriers in the Middle East due to war in the region was so acute that it dragged overall demand down -3.4%. The situation for air transport remains highly volatile,” Walsh said.

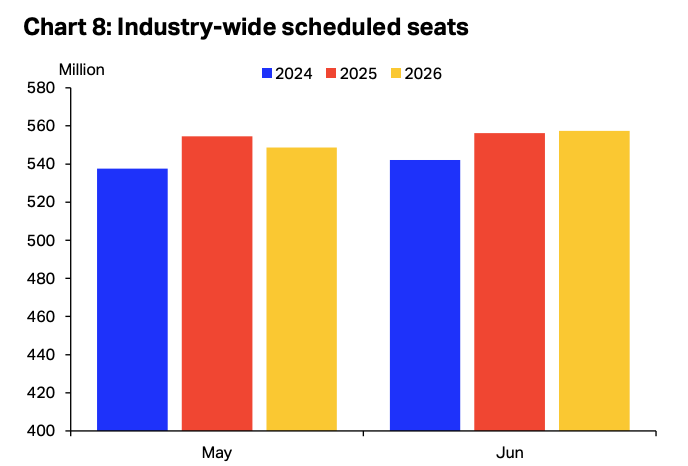

He went on to note that “The cost of jet fuel more than doubled in April, which is pushing airfares up. Forward schedule data is showing a reduced offering in the coming months, indicating that airlines are balancing high fuel costs and weaker demand.”

Monthly Statistics

Regional picture

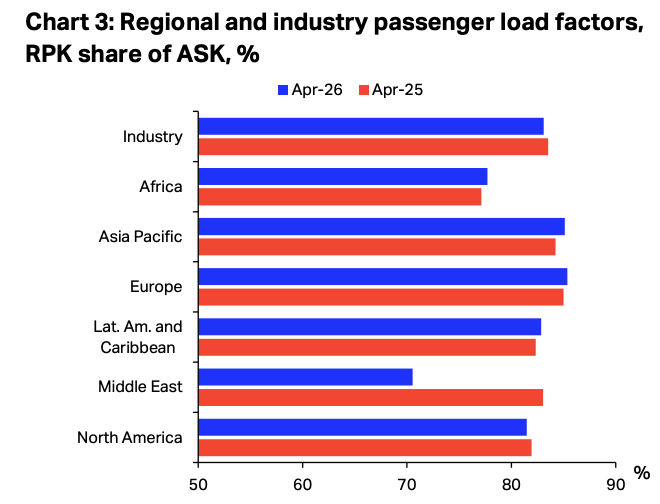

Regionally, international revenue passenger kilometres (RPK), which reflects real passenger traffic, fell by 5.3%, with capacity falling 5.1%. However, this decrease was caused by declining demand for Middle East carriers. Excluding the Middle East, RPK increased by 1.9%. North America was flat, and all other regions reported growth.

Against this backdrop, Asia-Pacific airlines achieved a three per cent year-on-year increase in demand. Capacity increased 0.7% year-on-year, and the load factor was 87.5% (+1.9 ppt compared to April 2025), a record high for April. There was a notable slowdown in traffic on the Japan-China corridor due to ongoing political tensions.

European carriers saw a 0.9% year-on-year increase in demand. Capacity increased 0.3% year-on-year, and the load factor was 84.9% (+0.6 ppt compared to April 2025). Direct traffic between Europe and Asia increased 15.3% as it replaced traffic transiting through the Middle East, the report said.

Monthly Statistics

North American carriers saw a 0.0% year-on-year increase in demand. Capacity decreased 1.1% year-on-year, and the load factor was 83.9% (+0.9 ppt compared to April 2025).

Middle Eastern carriers saw a -48.1% year-on-year decrease in demand. Capacity fell 38.4% year-on-year, and the load factor was 70.1% (-13.1 ppt compared to April 2025). Traffic was impacted by the ongoing Iran war, though the decline slowed a little compared to March, as an uneasy ceasefire came into effect.

Latin American airlines achieved an 8.9% year-on-year increase in demand. Capacity climbed 7.2% year-on-year. The load factor was 84.6% (+1.4 ppt compared to April 2025).

African airlines saw a 2.2% year-on-year increase in demand. Capacity was up 1.2% year-on-year. The load factor was 77.9% (+0.7 ppt compared to April 2025).

Domestic passenger markets

Domestic RPK was flat in April compared to April 2025. Growth in Brazil, China, and Japan was balanced out by falls in Australia, India, and the United States. Load factors fell in most of the major markets, barring China and Japan, though capacity in the Japanese market has declined for eight months in a row, the IATA pointed out.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}