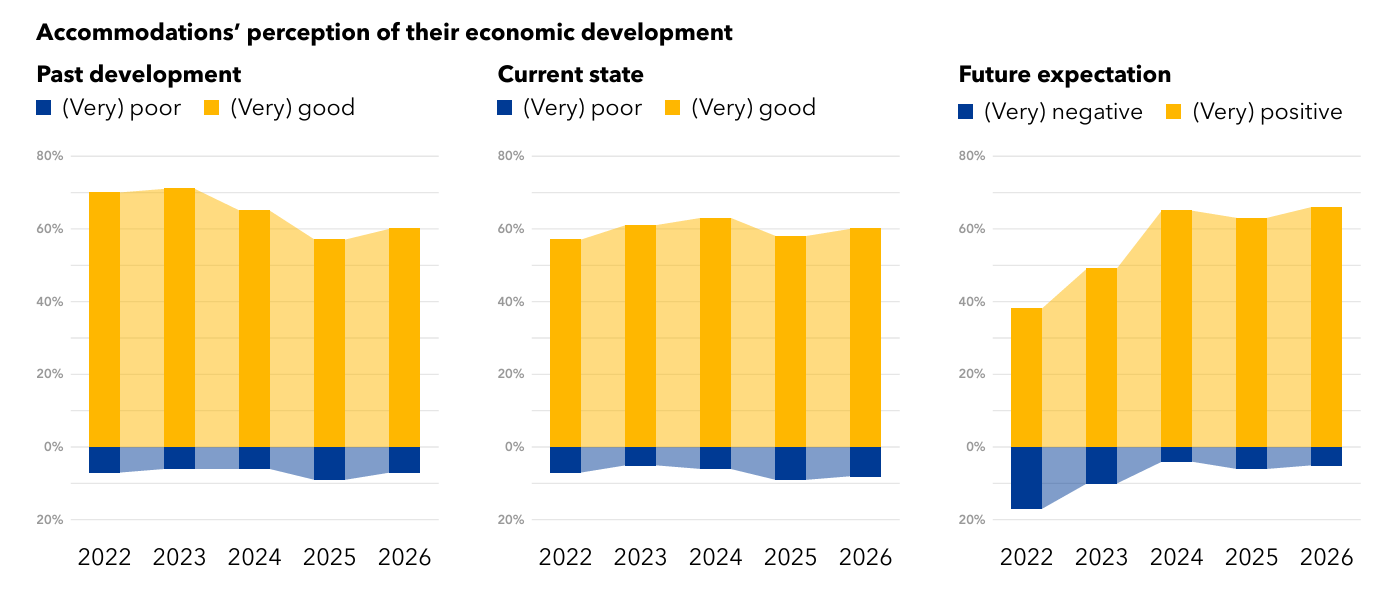

Booking.com has released the sixth edition of its European Accommodation Barometer, giving an overview of how accommodation providers across Europe view the current market and the year ahead. The report is based on responses from 1,240 executives and managers across 24 European markets in the hospitality sector. It shows an industry that continues to recover and adapt after several years of major disruption. Most businesses report a positive outlook, but the findings also show that not all parts of the sector are moving at the same pace. Differences between large hotel chains and independent properties are becoming more visible in both financial results and future expectations.

Overall sentiment in the European accommodation sector remains positive, with 66% of businesses expecting strong performance in the next tourism season. Around 60% say they are currently in a good financial position, which suggests a stable base for growth. Occupancy levels are also improving, with 50% of businesses reporting increases compared to the previous year. At the same time, 40% report higher average daily rates, which is slightly lower than in 2025 when 43% saw price increases. This shows that demand is still present, but price growth is becoming more moderate. The industry appears steady, but not evenly strong across all segments.

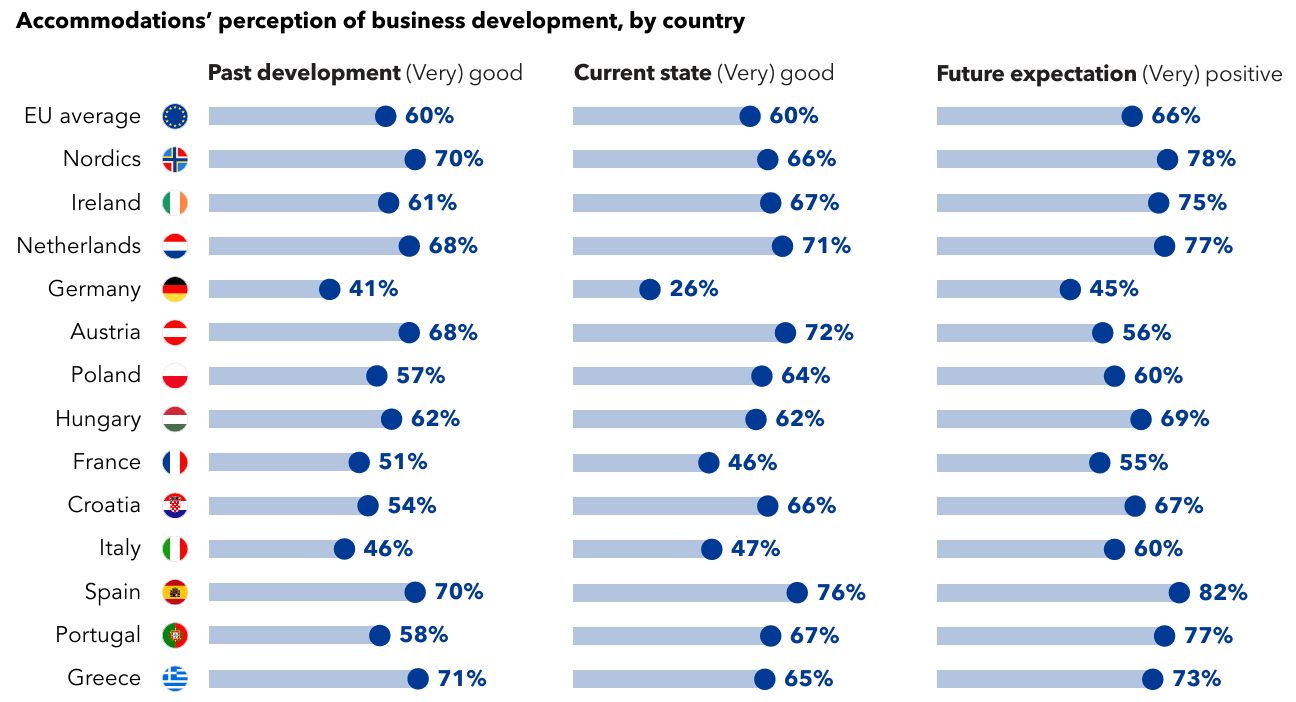

A key finding of the report is the widening gap between hotel chains and independent accommodation providers. Large chains consistently report stronger results across key indicators. Around 72% of hotel chains describe their financial situation as positive, compared to 55% of independent businesses. Performance differences also appear in room pricing and occupancy levels. About 47% of chains report higher room rates, while only 37% of independents see the same trend. In terms of occupancy, 56% of chains report growth compared to 46% of independent properties. These differences suggest that scale and resources are becoming more important in determining how well businesses perform in the current market.

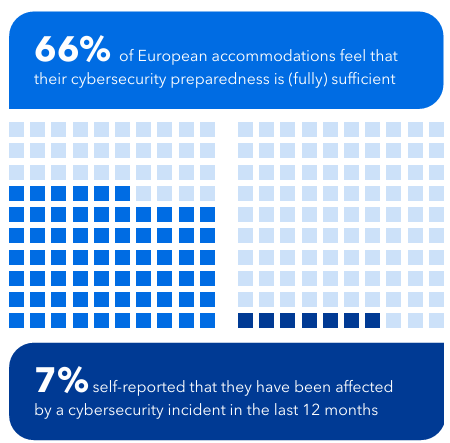

The report also highlights cybersecurity as one of the most important challenges facing the sector. Overall, 66% of European accommodation providers feel prepared to deal with cyber threats. However, this confidence is much higher among larger businesses. Almost all companies with more than 250 employees, at 94%, say they are well prepared, compared to only 60% of small businesses with fewer than ten employees. Smaller properties are also less likely to invest in staff training, regular system audits, and external cybersecurity support. Only 49% of small businesses offer cybersecurity training, compared to 89% of larger companies. This gap suggests that smaller operators may face more difficulty in keeping up with growing digital risks, especially as cyberattacks become more advanced and targeted.

Concerns about cyber threats are also reflected in expectations for the next tourism season. Around 21% of small businesses see cyberattacks as a major risk, compared to just 9% of larger companies. Payment fraud follows a similar pattern, with 25% of smaller businesses expressing concern compared to 16% of larger operators. While larger companies report more cybersecurity incidents overall, this likely reflects better monitoring systems and higher exposure due to scale. Smaller businesses, on the other hand, may experience fewer reported incidents but also have fewer tools to detect and respond to them.

Beyond digital risks, external disruptions are also shaping expectations for the coming year. Around 37% of accommodation providers are concerned about extreme weather events or natural disasters that could affect travel demand. In addition, 32% point to local disruptions such as transport strikes or infrastructure work that could limit access to destinations. These concerns show that external factors are becoming a regular part of business planning in tourism. Weather and transport issues are no longer seen as rare events but as ongoing risks that need to be managed throughout the year.

Managing seasonality remains a key priority across the sector. Around 72% of businesses offer discounts or special packages during off-peak periods to attract more guests. Online platforms are widely seen as effective tools for generating demand, with 81% of providers relying on them during low occupancy periods. Marketing strategies also include social media, used by 54% of businesses, paid advertising at 50%, email campaigns at 41%, and traditional media at 34%.

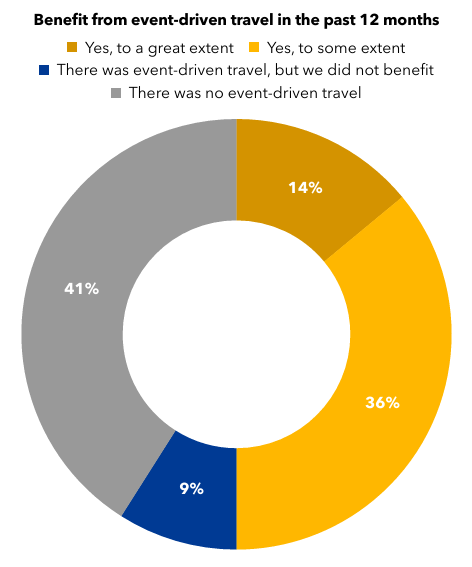

This mix shows that accommodation providers are using multiple channels to reach potential guests, rather than relying on a single approach. Event-driven tourism is also becoming more important, with 50% of businesses reporting benefits from events and special occasions. Among those, 66% saw higher revenue per available room, while 60% reported increased bookings during slower periods.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}