Global airlines are facing a steep rise in operating costs as conflict in the Middle East drives up fuel prices, forcing carriers to increase fares while seeing profits nearly halved.

Speaking at the International Air Transport Association (IATA) annual summit in Rio de Janeiro, airline leaders warned that although widespread jet fuel shortages are unlikely, the industry is being hit by a fuel cost shock worth almost $100 billion.

According to IATA’s latest financial outlook, airlines are expected to spend $350 billion on fuel in 2026, up from $252 billion in 2025. The increase comes despite global fuel consumption remaining broadly unchanged at around 104 billion gallons.

The sharp rise is entirely driven by higher prices. IATA forecasts jet fuel will average $152 per barrel this year, almost 70% higher than the $90 per barrel recorded in 2025. Crude oil prices are expected to average $95 per barrel, compared with $69 last year.

Profits cut almost in half

The higher fuel bill, combined with operational disruption caused by the war in the Middle East, has prompted IATA to dramatically downgrade its industry outlook.

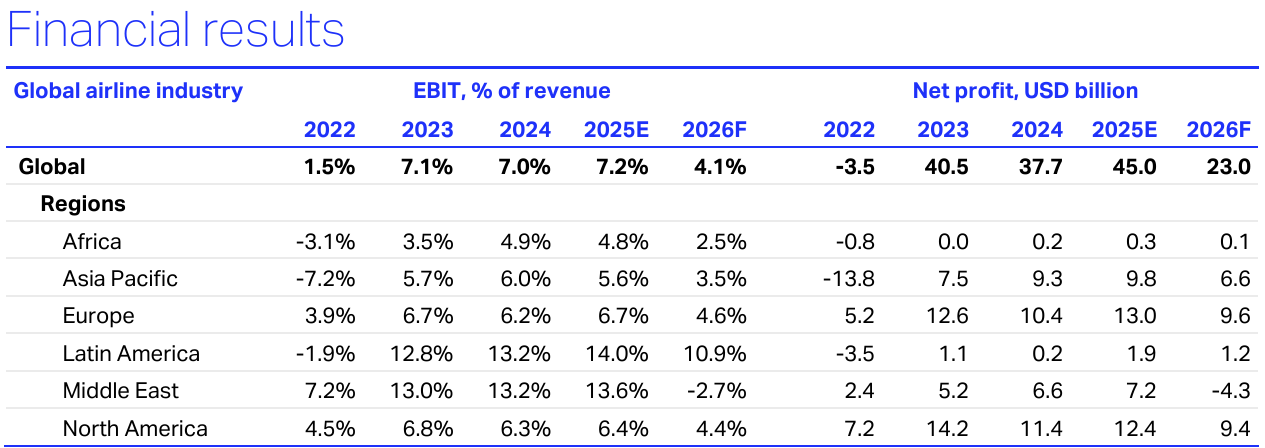

Global airlines are now expected to post a combined net profit of $23 billion in 2026, compared with a previous forecast of $41 billion. The figure is also roughly half the $45 billion profit generated in 2025.

Net profit margins are forecast to fall from 4.2% to just 2.0%, while net profit per passenger is expected to decline from $9.10 to $4.50.

“War-related disruptions in the Middle East and rising fuel costs have shifted the outlook for airlines to the worse,” said Willie Walsh, IATA’s Director General.

“Profits will shrink from $45 billion in 2025 to $23 billion this year. And margins will shrink from 4.2% to 2.0%.”

Walsh noted that all airline bottom lines are suffering from the rapid rise in fuel prices, even though some of the additional costs are being recovered through fare increases and efficiency measures.

Passengers likely to pay more

The latest figures suggest travellers should expect air fares to continue rising throughout the year.

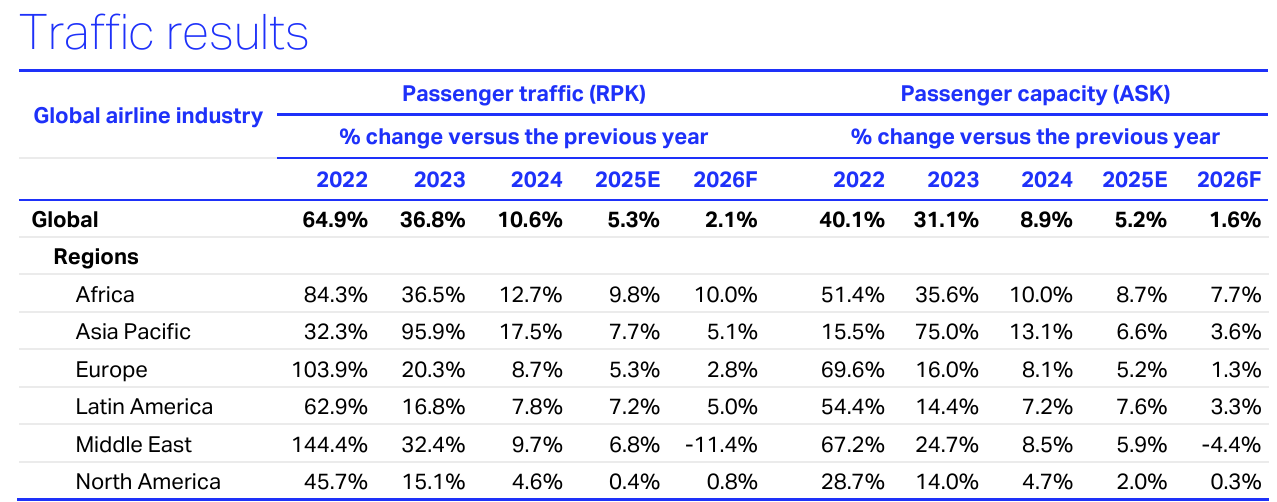

Passenger ticket revenues are forecast to increase by 9.2% to $839 billion, significantly outpacing expected passenger demand growth of 2.1%. Passenger yields, a key measure of average fare levels, are expected to rise by 7%.

IATA said airlines are actively attempting to recover part of the fuel shock through higher ticket prices, while also increasing ancillary revenues from services such as baggage, seat selection and onboard purchases.

“While air fares are rising, airlines are still absorbing part of the hike in their bottom lines,” Walsh said.

“Net profit per passenger is expected to fall to $4.50, half of what it was last year. Under the circumstances, that shows resilience.”

Despite higher prices, demand remains strong. Passenger numbers are expected to reach 5.1 billion in 2026, up 2.4% on last year, while average load factors are forecast to reach a record 84%, meaning airlines will fill more seats than ever before.

Middle East airlines hardest hit

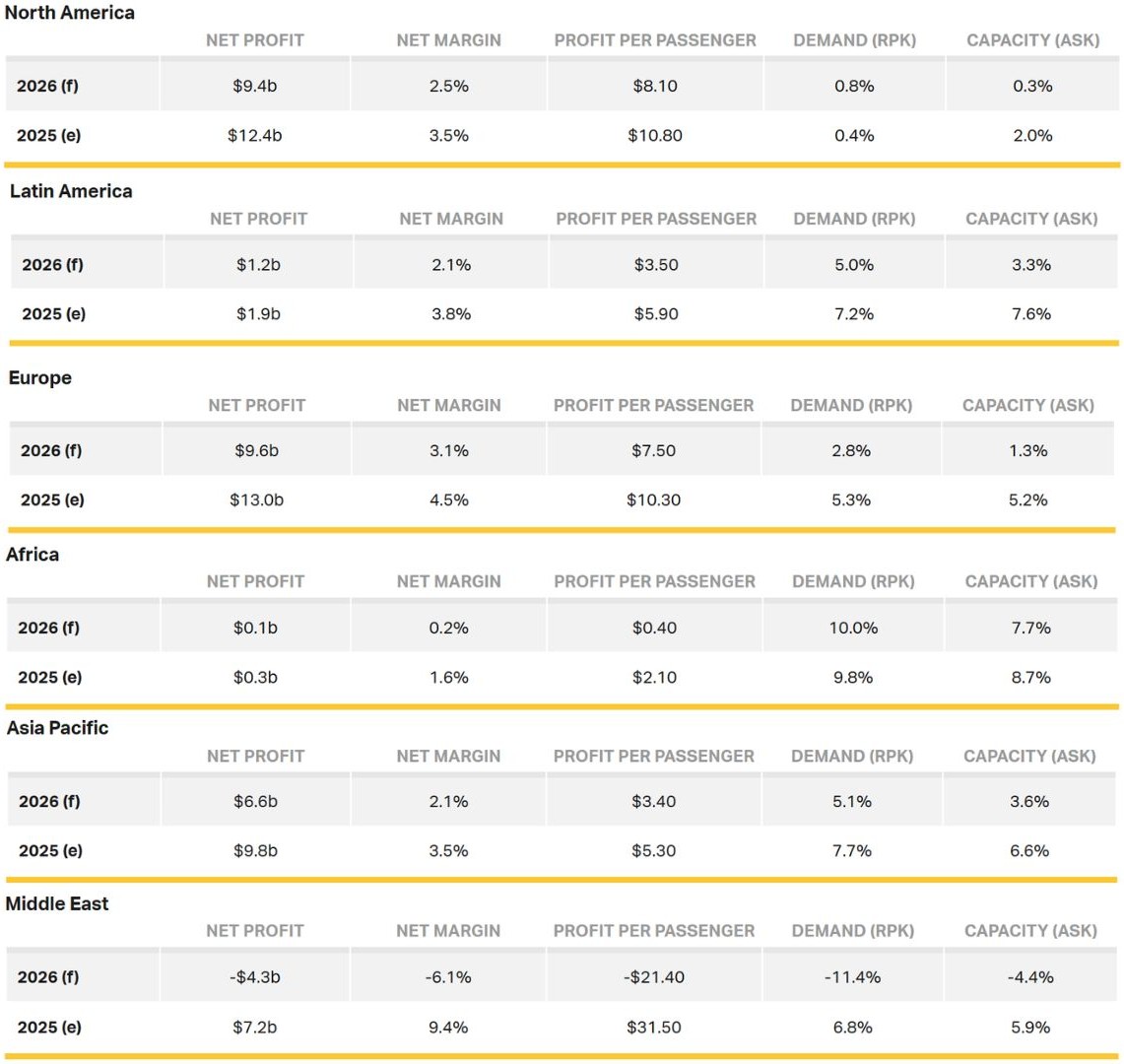

Airlines based in the Middle East are expected to suffer the most severe financial consequences.

The region, which generated a collective profit of $7.2 billion in 2025, is forecast to post a net loss of $4.3 billion in 2026. The conflict has disrupted key air corridors, forced airspace closures and weakened transfer traffic through major Gulf hubs.

“Gulf carriers face operational uncertainty following a near complete shutdown of airspace at the outbreak of the war,” Walsh said.

“These carriers are doing an amazing job maintaining connectivity, but major financial impacts are unavoidable.”

Elsewhere, airlines are expected to remain profitable, although at significantly lower levels than previously anticipated.

European airlines are forecast to generate $9.6 billion in profit, down from $13 billion last year, while North American carriers are expected to earn $9.4 billion, compared with $12.4 billion in 2025.

Aircraft shortages and rising costs

Fuel is not the only challenge facing the sector.

Airlines continue to struggle with aircraft delivery delays and supply chain disruptions. IATA said the global aircraft order backlog reached 18,100 aircraft in May 2026, representing more than half of the active fleet currently in service.

The shortage is forcing airlines to keep older aircraft flying longer, increasing maintenance costs and slowing progress on fuel efficiency improvements.

Aircraft lease rates have also reached record highs as airlines compete for limited capacity.

Additional pressures come from labour costs, sustainability regulations and investments in cleaner fuels. The airline industry is expected to spend an extra $4.3 billion on Sustainable Aviation Fuel (SAF) this year, while carbon offsetting obligations under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) are estimated to cost up to $1.6 billion.

Travellers remain optimistic

Despite geopolitical tensions and rising prices, passenger confidence remains remarkably resilient.

An IATA survey of 6,500 travellers across 15 countries found that 41% expect to travel more over the next 12 months, while a further 52% plan to travel at similar levels.

Although 83% of respondents said they were becoming more cost conscious, most still view air travel as good value for money.

For airlines, however, the challenge remains balancing strong demand with mounting costs. With fuel now accounting for more than 31% of total operating expenses, up from 25% last year, the industry faces a difficult year ahead as it seeks to absorb the biggest fuel price shock in more than a decade.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}